Financial institutions are not experimenting with AI chatbots anymore. They are deploying them in production, measuring ROI, and expanding use cases across every segment of the business. The question for banking executives, CIOs, and digital transformation leaders is no longer whether to invest. It is how to build, govern, and scale these systems responsibly.

This guide covers everything you need to make that decision with clarity: the business case, the technology architecture, 12 proven enterprise use cases, segment-specific applications, implementation roadmap, compliance requirements, common failure modes, and a pre-deployment checklist. Every major claim is grounded in named research.

Why Financial Institutions Are Investing in AI Chatbots

Direct answer: Financial institutions are investing in AI chatbots for three converging reasons: rising customer expectations for 24/7 digital support, significant operational cost pressure, and the measurable productivity gains now visible in early enterprise deployments.

The market numbers reflect the urgency. The global generative AI in financial services market was valued at $2.2 billion in 2024 and is projected to reach $25.7 billion by 2033, growing at a compound annual growth rate of 30.3% (Grand View Research, 2025). The broader conversational AI market reached $11.58 billion in 2024 and is forecast to hit $41.39 billion by 2030 (K2View, 2024).

These are not speculative projections. They track real deployment activity.

According to McKinsey, AI and analytics applied to global banking could generate annual value as high as $1 trillion. A separate McKinsey analysis found AI is expected to reduce costs by 20% for financial institutions. Accenture estimates that 73% of the time spent by US bank employees has a high potential to be impacted by generative AI, with 39% automatable and 34% augmentable.

The productivity case is equally strong at the individual level. Research from the National Bureau of Economic Research found that customer support professionals given access to AI assistance increased their productivity by an average of 14%. IBM’s Institute for Business Value (2025) found that mature AI adopters in customer service reported 38% lower average inbound call handling time and 17% higher customer satisfaction.

Despite these results, adoption gaps remain. A Deloitte survey of 2,027 US bank customers conducted in January 2025 found that 37% of respondents had never interacted with a banking chatbot. This is not a sign that demand is low. It is a sign that the opportunity is large and the competitive window is still open.

What Are AI Chatbots for Financial Services?

Direct answer: AI chatbots for financial services are software systems that use large language models, natural language processing, and enterprise data retrieval to conduct conversations with customers or employees, answer questions, execute transactions, and automate workflows within regulated financial environments.

The term covers a range of technical sophistication.

A rule-based chatbot follows scripted decision trees. It handles a narrow set of predefined questions and routes everything else to a human agent. These systems are inexpensive to build but frustrating to use. They are largely what gave early banking chatbots a poor reputation.

A conversational AI chatbot uses natural language processing and machine learning to understand intent, manage multi-turn conversations, and handle a broader range of queries without predefined scripts.

A generative AI chatbot powered by an LLM generates responses based on reasoning over retrieved information. These systems handle nuanced questions, explain complex financial products, summarize documents, and adapt tone and detail level to the user’s needs.

A RAG-powered enterprise chatbot adds Retrieval-Augmented Generation to the LLM layer. Instead of generating responses from model training data alone, the system searches your internal knowledge base, retrieves verified documents, and grounds every response in your actual policies, products, and procedures. This distinction matters enormously in financial services, where accuracy is a compliance requirement.

One of the most common misconceptions among financial institutions evaluating AI chatbots is that the LLM itself determines quality. In practice, the retrieval architecture, the quality of the underlying knowledge base, and the governance controls around the system have a greater impact on production performance than model selection.

A chatbot connected to outdated product documentation will produce inaccurate answers regardless of which model powers it.

Benefits of AI Chatbots for Financial Services

Faster customer support

AI chatbots respond instantly, around the clock, without queue times. IBM’s case study of a UK retail and commercial bank found that implementing conversational AI for customer queries resulted in a 150% boost in satisfaction for certain interaction types. The speed improvement is not marginal. Customers who receive a correct answer in 10 seconds behave differently from customers who wait 8 minutes for a human agent.

Reduced operational costs

A human-handled customer service interaction in financial services costs several dollars once salary, overhead, and management are factored in. An AI-handled interaction costs a fraction of that amount. Juniper Research projected that chatbot-driven cost savings in banking would reach $7.3 billion annually by 2023. That figure has grown as deployment scale has increased.

Improved customer experience

Deloitte’s 2025 banking chatbot research found that chatbot users favor them primarily for quick responses (78%) and ability to handle simple queries (69%). When the interaction design is good and the underlying knowledge is accurate, customer satisfaction improves materially.

Higher employee productivity

AI chatbots are not only customer-facing. Internal employee helpdesk bots reduce the time HR, IT, and operations teams spend answering repetitive internal queries. McKinsey’s 2023 research found that knowledge workers spend an average of 19% of their working week searching for and gathering information. Internal AI assistants directly address this cost.

Scalability without proportional headcount

A chatbot handling 500 simultaneous conversations costs roughly the same to operate as one handling 50. Human support teams cannot scale at the same rate or the same cost curve. This distinction becomes critical during peak periods: tax season, market volatility events, product launches, and regulatory changes.

Compliance and audit support

Well-architected AI chatbots generate detailed conversation logs, maintain audit trails, and route sensitive decisions to human reviewers. This creates a compliance infrastructure that manual processes rarely achieve consistently.

12 Enterprise Use Cases for AI Chatbots in Financial Services

1. Customer support

Handling balance inquiries, account status checks, transaction history, and branch or ATM locators. These interactions represent the highest volume of inbound contacts for most retail banks and are the clearest starting point for chatbot deployment.

2. Account information

Providing real-time account details, statement summaries, pending transactions, and recent activity explanations. When integrated with core banking APIs, chatbots deliver personalized responses rather than generic answers.

3. Card management

Processing card block or unblock requests, reporting lost or stolen cards, managing spending limits, and explaining transaction disputes. These are high-urgency interactions where 24/7 availability has direct customer satisfaction impact.

4. Loan assistance

Answering questions about loan products, eligibility criteria, required documentation, and application status. Deloitte’s 2025 research noted that banks can expand chatbot use into loan processing and application support as AI systems mature beyond basic functionality.

5. Mortgage applications

Guiding applicants through documentation requirements, explaining loan-to-value ratios, answering questions about interest rate types, and providing application status updates. Mortgage processes are document-heavy and time-sensitive, making them strong candidates for AI assistance.

6. Fraud detection alerts

Notifying customers of suspicious transactions, collecting confirmation or denial responses, and triggering escalation workflows when fraud is confirmed. Real-time fraud communication reduces both financial losses and customer anxiety.

7. KYC support

Guiding customers through Know Your Customer documentation requirements, explaining what is needed and why, and tracking submission status. KYC processes are a significant friction point in onboarding. Chatbots reduce drop-off rates.

8. Investment assistance

Answering questions about investment products, explaining portfolio performance, summarizing market data, and routing advisory requests to licensed professionals. Only 27% of respondents in Deloitte’s 2025 survey trust AI for financial advice, which means human escalation paths remain essential for this use case.

9. Internal employee helpdesk

Answering HR policy questions, IT support requests, compliance procedure queries, and benefits information. Internal bots reduce the volume of repetitive requests hitting HR, IT, and compliance teams without customer-facing regulatory exposure.

10. Insurance claims processing

Walking customers through claim submission, tracking claim status, explaining coverage terms, and escalating disputed claims. This use case is particularly valuable in property and casualty insurance where claim volume spikes after weather events.

11. Compliance assistance

Helping employees understand regulatory requirements, locate relevant policy documents, check procedure compliance, and document decisions. Compliance AI assistants reduce regulatory risk when built with appropriate guardrails.

12. Personalized financial recommendations

Surfacing relevant products based on account behavior, spending patterns, and stated financial goals. This use case requires careful governance: every recommendation must be explainable, auditable, and compliant with applicable financial advice regulations in the target jurisdiction.

AI Chatbots Across Financial Segments

Retail banking

Retail banking generates the highest chatbot interaction volume. Common applications include account servicing, card management, loan inquiries, and fraud alerts. The Deloitte 2025 survey found that banking customers use chatbots most frequently for technical support (60%) and account inquiries (53%). Retail banking chatbots must handle high concurrency, integrate with core banking platforms, and maintain seamless handoffs to human agents.

Investment banking

Use cases in investment banking center on internal productivity: research summarization, document analysis, regulatory filing support, and due diligence assistance. Client-facing applications in this segment require careful compliance controls around financial advice regulations.

Insurance

Insurance chatbots handle claims first notice of loss, policy inquiries, coverage explanations, premium calculations, and renewal reminders. Document-heavy workflows, including policy documents and claims forms, benefit significantly from LLM-powered summarization and extraction.

FinTech

Fintechs often build AI chatbots earlier and faster than traditional banks because they carry less legacy infrastructure debt. Common use cases include onboarding assistance, transaction explanation, budgeting guidance, and customer retention workflows.

Wealth management

Wealth management chatbots support advisors rather than replacing them. They summarize client portfolios, surface relevant research, prepare meeting briefs, and draft client communications for advisor review. The human advisor remains central; the chatbot reduces preparation time.

Credit unions

Credit unions face the same customer service expectations as large banks with smaller technology budgets. AI chatbots offer credit unions a way to extend service hours and handle routine inquiries without proportional staffing increases.

Architecture of an Enterprise Banking Chatbot

Direct answer: A production-grade banking chatbot requires seven layers working together: user interface, authentication, business logic and orchestration, LLM integration, RAG retrieval pipeline, enterprise system integrations, and monitoring and compliance controls.

The data flow works as follows:

| Layer | Component | Function |

|---|---|---|

| User interface | Web chat, mobile app, voice channel | Receives user input |

| Authentication | SSO, OAuth, MFA | Verifies user identity and permissions |

| Business logic | Backend API (Python/FastAPI, Node.js) | Orchestrates requests, applies rules |

| LLM integration | GPT-4, Claude, or equivalent | Generates responses from retrieved context |

| RAG pipeline | Vector database (Pinecone, pgvector) | Retrieves relevant documents before generation |

| Enterprise integrations | Core banking, CRM, compliance, fraud systems | Provides live data for accurate responses |

| Monitoring and audit | Logging, alerting, conversation analytics | Tracks quality, security, and compliance |

One architectural decision determines more of the outcome than any other: whether you build with RAG. A chatbot without RAG generates responses from the LLM’s training data. That data does not include your current product terms, your specific policies, your regulatory disclosures, or your customer account information. The result is confident-sounding responses that are frequently wrong in precisely the details that matter most in financial services.

RAG systems reduce hallucinations by 70 to 90% compared to standard model inference (Makebot.ai, 2024). For financial services, this is not an optional performance improvement. It is the difference between a compliant system and a regulatory liability.

Challenges of Deploying AI Chatbots in Financial Services

Financial services face challenges that consumer AI deployments do not. Understanding them before development begins is not pessimism. It is how you avoid the most expensive surprises.

Hallucinations and accuracy. LLMs generate plausible text. They do not inherently verify facts. In financial services, an inaccurate response about interest rates, coverage terms, or regulatory requirements can cause real harm. RAG architecture, output validation, and human-in-the-loop workflows for high-stakes interactions are the primary mitigations.

Regulatory compliance. Banking chatbots operate under GDPR, PCI DSS, MiFID II, Basel III, CCPA, and jurisdiction-specific financial advice regulations. Non-compliance is not a technical debt problem. It is a legal and reputational risk. Compliance should be designed in from Phase 1.

Legacy system integration. Most banks run core banking platforms that were not designed for API-first integration. Connecting AI chatbots to these systems adds development time, requires middleware in many cases, and introduces integration maintenance overhead that must be planned for.

Customer trust. Deloitte’s 2025 survey found 74% of banking customers still prefer human agents over chatbots for routine interactions, and only 27% trust AI for financial advice. Trust is built through accuracy, transparency about AI involvement, and reliable escalation to human agents.

Security and data exposure. Chatbots that access customer account data create new attack surfaces. Prompt injection, unauthorized data retrieval, and session vulnerabilities all require explicit mitigation.

Governance and oversight. Without defined ownership, audit trails, and escalation procedures, AI chatbots in financial services create accountability gaps that regulators will not accept.

Security and Compliance for Banking Chatbots

Direct answer: Banking chatbots must be designed to meet GDPR, PCI DSS, SOC 2 Type II, and ISO 27001 requirements as a baseline. Compliance retrofitted after deployment costs more and achieves less than compliance designed in from the start.

The following controls are non-negotiable for production financial services deployments:

Encryption. All data must be encrypted at rest and in transit using current industry standards. PCI DSS requires that cardholder data never be stored in chatbot conversation logs.

Role-based access control. A retail customer’s chatbot session must not be able to retrieve another customer’s account data. An employee chatbot must enforce department-level document permissions. Access must be granted by role, not by trust.

Audit trails. Every conversation, every document retrieved, every action taken, and every API call made must be logged with timestamps and user identifiers. In regulated industries, audit trails are not operational niceties. They are compliance requirements.

Prompt injection protection. OWASP’s LLM Top 10 (2025) lists prompt injection as the highest-priority security risk for AI applications. In a banking context, a successful prompt injection attack could cause the system to reveal customer account data, bypass authorization controls, or execute unintended transactions. Input validation, prompt isolation, and output filtering are the primary defenses.

Human review requirements. High-stakes outputs including financial advice, transaction approvals, fraud determinations, and regulatory decisions must route to human review before action. Automated decisions in these categories create unacceptable regulatory exposure.

Data residency. GDPR and equivalent regulations in many jurisdictions require customer data to remain within specific geographic boundaries. Cloud deployment architecture must account for this from the infrastructure design stage.

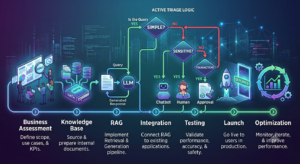

AI Chatbot Implementation Roadmap for Financial Services

Step 1: Business assessment

Define the specific problem you are solving and the outcome you will measure. “We want an AI chatbot” is not a business objective. “We want to reduce tier-1 support call volume by 30% within 12 months” is. The measurable target drives every architectural decision that follows.

Step 2: Use case selection

Start with one use case that meets three criteria: high volume of repetitive interactions, low regulatory complexity, and clear success metrics. Account inquiry handling or card management are typical starting points. Multi-use-case launches increase coordination complexity without improving the probability of success.

Step 3: Knowledge base preparation

Audit all documentation the chatbot will use: product FAQs, policy documents, regulatory disclosures, procedure manuals, and compliance guides. Remove outdated content. Resolve contradictions. Structure information consistently. Poor data quality is the most common cause of poor chatbot performance in production. Improving data before development delivers more value than refining prompts after launch.

Step 4: RAG pipeline design

Define the retrieval architecture. Select a vector database. Design chunking strategy for documents. Build the embedding pipeline. Test retrieval quality against real user queries before connecting the LLM layer. The retrieval pipeline deserves more engineering attention than most teams allocate to it.

Step 5: Enterprise system integration

Identify which systems the chatbot must access to answer accurately: core banking platform, CRM, compliance management system, fraud detection, and product catalog. Map the API landscape. Identify systems without clean APIs and estimate middleware requirements. Integration complexity has a greater impact on timelines than LLM integration itself.

Step 6: Security and compliance build

Implement authentication, role-based access, encryption, audit logging, and prompt injection protections before testing with real users. Do not treat these as post-launch improvements.

Step 7: Testing and validation

Test against accuracy, hallucination rate, security vulnerabilities, latency, conversation quality, and escalation behavior. Use real queries from current support logs, not synthetic scenarios. Real user queries expose failure modes that internal testing misses.

Step 8: Phased deployment and continuous optimization

Launch to a defined user segment. Monitor performance against your baseline metrics weekly. Update knowledge base as products and policies change. Schedule optimization cycles before performance degrades rather than in response to it.

How to Choose an AI Chatbot Development Partner for Financial Services

Not every AI development firm has the experience to build compliant, production-grade chatbots for regulated financial environments. Evaluate potential partners against these criteria:

| Evaluation Criterion | What to Look For |

|---|---|

| Financial services experience | Prior production deployments in banking, insurance, or fintech |

| Compliance knowledge | Demonstrated understanding of GDPR, PCI DSS, SOC 2 |

| RAG and LLM architecture | Proven RAG implementations, not just API integrations |

| Enterprise integration capability | Experience with core banking systems and legacy middleware |

| Security practices | OWASP-aligned testing, penetration testing methodology |

| Post-launch support | Defined monitoring, optimization, and knowledge update processes |

| Long-term governance | Approach to model updates, drift monitoring, and auditability |

A development partner who cannot explain how they would mitigate prompt injection in a banking context is not ready for financial services deployment.

Enlight Lab’s AI Chatbot Development Services are designed specifically for enterprise environments where compliance, integration complexity, and long-term governance determine whether a deployment succeeds. Our AI Consulting Services can help you assess use case readiness and design a deployment roadmap before development begins.

Common Mistakes When Deploying Banking AI Chatbots

One of the most consistent patterns across failed financial services AI projects is that the technical failure is usually a symptom of a planning failure. These are the mistakes we see most frequently:

Building without defined governance. A chatbot with no defined owner, no escalation procedures, and no review cadence will generate compliance problems. Governance is not a project phase. It is an ongoing operational responsibility.

Ignoring compliance until launch. Retrofitting data residency controls, audit logging, and access management after a system is live costs more in rework than building them in from the start.

Poor knowledge base quality. The chatbot will answer based on what it retrieves. Outdated FAQs, contradictory policy documents, and unstructured content produce inaccurate responses regardless of which LLM is used.

Skipping RAG. Relying on LLM training data alone in financial services is not a technical shortcut. It is a compliance risk. The model does not know your current rates, your current terms, or your current regulatory disclosures.

No human escalation path. Deloitte’s 2025 research found that 74% of banking customers still prefer human agents for many interactions. A chatbot without a clear, low-friction escalation path produces frustrated customers and reputational damage.

No monitoring after launch. Production AI systems drift. Knowledge becomes outdated. User behavior changes. Retrieval quality degrades as documentation grows. Teams that do not monitor continuously discover problems through customer complaints rather than analytics.

Choosing the wrong LLM for the workload. The most powerful model is not always the right choice. High-volume, low-complexity queries served by an over-specified model waste infrastructure budget. Model selection should match the complexity distribution of actual user queries.

Enterprise AI Chatbot Pre-Deployment Checklist

Before deploying an AI chatbot in a financial services environment, confirm the following:

- Business objective is defined with a specific, measurable outcome

- Use case selected meets the criteria of high volume, manageable regulatory complexity, and clear success metrics

- Knowledge base has been audited, cleaned, and structured

- RAG pipeline has been tested against real user queries, not synthetic scenarios

- Authentication and role-based access control are implemented and tested

- Data encryption is applied at rest and in transit

- Audit logging captures all conversations, retrievals, and API calls

- Prompt injection protections are in place and tested against OWASP LLM Top 10 vectors

- Human escalation path is defined and tested

- Compliance requirements (GDPR, PCI DSS, applicable local regulations) have been reviewed and addressed

- Incident response procedure is documented and assigned

- Performance monitoring dashboard is live before user traffic begins

- Post-launch optimization schedule is defined

What is the ROI of AI chatbots in financial services?

ROI varies by use case and deployment quality. IBM’s IBV (2025) data shows mature AI adopters in customer service achieve 38% lower average call handling times and 17% higher customer satisfaction. McKinsey estimates AI will reduce costs by 20% for financial institutions. The most reliable ROI projections come from measuring a specific baseline metric before deployment and tracking it against your chatbot’s actual performance after launch.

Building AI Chatbots for Financial Services That Actually Work

The financial services institutions that are generating measurable returns from AI chatbots share three characteristics: they started with a clearly defined business problem, they invested in data quality and retrieval architecture before writing prompts, and they treated deployment as the beginning of the lifecycle rather than the end.

The technology is mature enough to build on. The market is growing fast enough to reward early movers. The compliance requirements are demanding but navigable with the right architecture and the right partner.

The most common reason AI chatbot deployments underperform in financial services is not a problem with the underlying model. It is a problem with data quality, retrieval design, integration architecture, or governance. Organizations that solve these foundational problems before selecting a model consistently outperform those that do not.

If you are evaluating AI chatbot development for your financial services organization, Enlight Lab builds production-grade conversational AI systems designed for regulated industries. Our AI Chatbot Development Services cover architecture, RAG implementation, enterprise integration, compliance design, and post-launch optimization. Our Enterprise AI Strategy Roadmap service helps you prioritize use cases, assess your data readiness, and build an implementation plan before any development budget is committed.